If you’re buried in bills, juggling high-interest credit cards, or simply losing control of your monthly budget, you’re not alone. Millions of Americans face similar struggles—and for many, the best first step toward financial recovery is seeking help from a credit counseling service.

But when is the right time to consider it? What can credit counselors actually do for you? And how do you know if it’s worth it?

This in-depth guide explains when you should consider credit counseling services, what they offer, and how to decide whether it’s the right fit for your financial future.

What Are Credit Counseling Services?

Credit counseling is a free or low-cost service offered by nonprofit organizations to help individuals manage their debts, create budgets, and develop long-term financial plans. These services are typically provided by certified credit counselors trained in areas like consumer credit, debt management, and financial education.

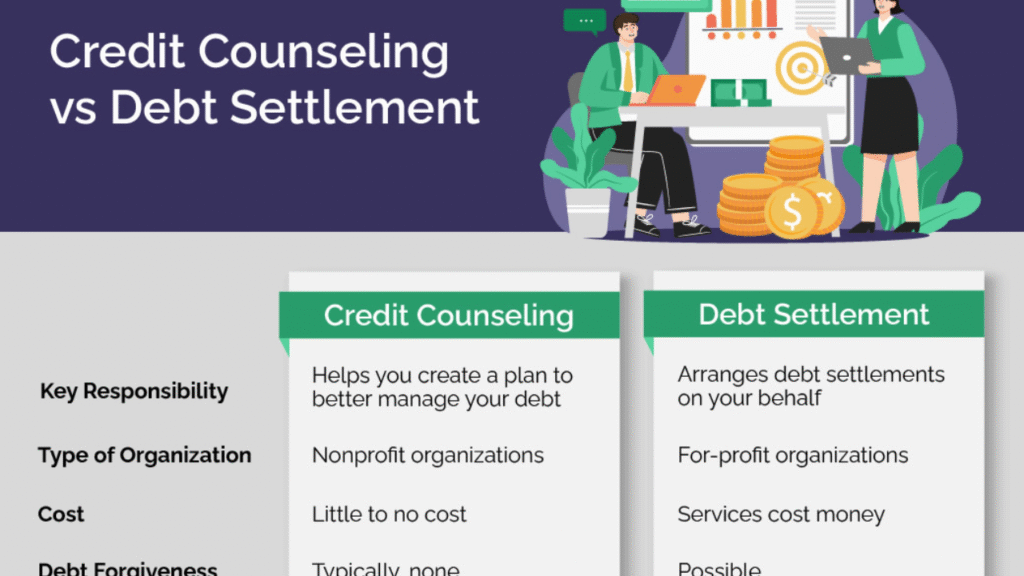

Credit counseling is not debt settlement. It doesn’t promise to slash your debt overnight. Instead, it focuses on practical, ethical, and sustainable solutions to help you regain financial control.

What Services Do Credit Counselors Provide?

| Service Offered | Description |

|---|---|

| Budget Counseling | Review of income, expenses, and financial goals |

| Debt Management Plans (DMPs) | Consolidated payments and lower interest rates through creditor negotiation |

| Credit Report Reviews | Help interpreting your credit reports and scores |

| Financial Education | Resources and tools to build healthy financial habits |

| Housing and Bankruptcy Counseling | Certified sessions for mortgage or bankruptcy-related issues |

When Should You Consider Credit Counseling Services?

Credit counseling isn’t just for people in crisis—it’s for anyone who wants to improve their financial outlook. However, there are specific scenarios where it can be especially helpful:

1. You’re Only Making Minimum Payments on Credit Cards

If your balance never seems to drop, and you’re stuck in a cycle of interest-only payments, a credit counselor can help you design a debt reduction strategy or enroll in a Debt Management Plan (DMP).

2. You’re Constantly Behind on Bills

Falling behind on rent, utilities, or credit cards month after month? Credit counseling helps identify spending leaks and structure your income to prioritize critical expenses.

3. You’re Considering Bankruptcy

Before filing, counseling is legally required. But more importantly, a credit counselor can help you explore alternatives that may preserve your credit and assets.

4. You Feel Overwhelmed by Debt Collectors

Constant calls from collectors are more than just annoying—they’re a sign your debt is spinning out of control. Credit counseling can create a plan to deal with creditors directly, reducing stress and harassment.

5. You Want to Build Better Financial Habits

Even if you’re not in a deep financial hole, credit counseling offers valuable tools for budgeting, saving, and improving your credit score.

Advantages of Credit Counseling

| Benefit | Explanation |

|---|---|

| Nonjudgmental, Professional Help | Counselors are trained, certified, and ready to help—not to shame |

| Personalized Financial Plans | Plans tailored to your income, goals, and lifestyle |

| Creditor Negotiation | Lower interest rates or fees via DMPs with creditor cooperation |

| Education Resources | Access to budgeting tools, webinars, and financial planning material |

| Improves Credit Over Time | Consistent payment plans can slowly rebuild your credit |

Possible Limitations to Consider

While credit counseling offers valuable help, it’s not perfect for every situation. Consider these factors:

- Debt Management Plans (DMPs) may require you to close credit accounts, which could affect your credit score in the short term.

- DMPs typically don’t include secured debts like mortgages or auto loans—only unsecured debts like credit cards.

- Not all counselors are nonprofit or trustworthy—some may charge high fees or offer biased advice.

Overview Table: When to Consider Credit Counseling

| Situation | Recommended Action Through Counseling |

|---|---|

| Struggling with minimum payments | Enroll in DMP to consolidate and lower interest |

| Facing calls from debt collectors | Get help negotiating with creditors |

| Budget constantly off balance | Receive professional budgeting advice and planning |

| Thinking about bankruptcy | Explore alternatives and fulfill required counseling |

| Want to improve financial literacy | Access free educational resources and tools |

| Afraid to face debt alone | Receive confidential, supportive, and professional guidance |

How to Choose a Reputable Credit Counseling Agency

- Ensure It’s Nonprofit

Look for agencies recognized by the National Foundation for Credit Counseling (NFCC) or the Financial Counseling Association of America (FCAA). - Check Accreditation

Verify credentials with the Better Business Bureau (BBB) and confirm that counselors are certified. - Watch for Red Flags

Avoid companies that:- Charge high upfront fees

- Promise quick fixes

- Push specific products (like debt settlement)

- Lack transparency about services

- Get a Free Consultation First

Most reputable agencies offer free initial sessions. Use this to ask questions, evaluate their professionalism, and make an informed decision.

Credit Counseling vs Other Options

| Option | Best For | Key Difference |

|---|---|---|

| Credit Counseling | Budgeting and moderate debt | Focus on education and long-term planning |

| Debt Settlement | Severe debt and inability to pay full | Negotiates lower payoff, harms credit |

| Debt Consolidation Loan | Good credit and stable income | Combines debts into one payment at lower interest |

| Bankruptcy | Extreme financial hardship | Legal process to discharge or restructure debt |

Final Thoughts

Credit counseling is not just for people in deep debt—it’s a smart and accessible tool for anyone seeking financial clarity, control, and confidence. Whether you’re on the verge of bankruptcy or just want to stop living paycheck to paycheck, a certified credit counselor can guide you through your options with empathy and expertise.

3 Best One-Line FAQs

Q: Does credit counseling affect your credit score?

A: No, credit counseling itself doesn’t impact your score—though a Debt Management Plan may affect it short-term.

Q: Are credit counseling services free?

A: Many nonprofit agencies offer free consultations, with minimal fees for ongoing plans like DMPs.

Q: Can credit counseling help with all types of debt?

A: It’s best for unsecured debt like credit cards, not secured loans like mortgages or car loans.